Creating a monthly budget does not have to be complicated to be effective. The 50/30/20 framework is a simple way to organize your money without tracking every dollar in detail. It focuses on balance, flexibility, and long-term stability rather than strict rules. Understand how the 50/30/20 budget works, how to apply it to real life, and how to adjust it so it supports your financial goals instead of adding stress.

What the 50/30/20 Framework Means

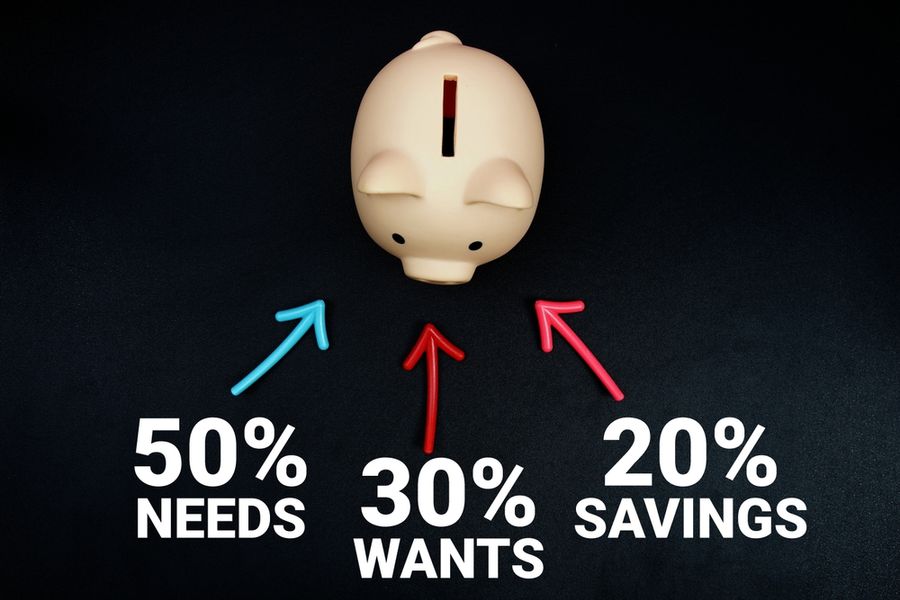

The 50/30/20 framework divides your after-tax income into three broad categories. Fifty percent goes toward needs, thirty percent goes toward wants, and twenty percent goes toward saving or debt reduction. Needs are expenses you must pay to live and work, wants are optional lifestyle expenses, and savings covers future-focused goals.

This framework is not meant to be perfect or rigid. It is a starting structure that helps you see where your money goes and whether it aligns with your priorities. The strength of this method is that it creates boundaries without requiring detailed spreadsheets or constant tracking.

Step One: Identify Your Monthly Income

Start by figuring out how much money you bring home each month after taxes and deductions. Use your regular take-home pay if your income is steady. If your income changes month to month, use a conservative average so your budget stays realistic.

Only include money you can count on. Bonuses, gifts, or irregular income can be treated as extra rather than part of the core budget. Once you know your monthly income, you can apply the 50/30/20 percentages with more confidence and avoid planning based on money that may not arrive.

Step Two: Define Needs vs Wants Clearly

One of the hardest parts of budgeting is separating needs from wants. Needs include housing, basic utilities, groceries, insurance, transportation required for work, and minimum debt payments. These are expenses that support daily living and cannot be skipped easily.

Wants are expenses that improve comfort or enjoyment but are not required. These include dining out, entertainment, subscriptions, hobbies, and upgrades. The goal is not to remove wants, but to keep them within a clear limit. Being honest about this distinction makes the framework work as intended.

Step Three: Apply the Percentages to Your Spending

Once you understand your income and expenses, group your current spending into the three categories. Compare what you spend now to the 50/30/20 targets. Many people discover that needs take up more than half of their income, which is common and not a failure.

If your needs exceed fifty percent, focus on awareness rather than immediate change. Look for small adjustments over time, such as lowering one bill or reducing an expense gradually. If wants exceed thirty percent, that area often offers more flexibility for short-term changes.

Step Four: Build the Savings and Debt Portion

The twenty percent category is for future progress. This includes emergency savings, retirement contributions, and extra payments toward debt beyond the minimums. If you are paying off debt aggressively, debt reduction can take priority within this category.

If saving twenty percent feels out of reach, start smaller and build up. Even consistent progress below the target helps create momentum. The key is treating savings and debt payoff as non-optional parts of your budget rather than leftovers.

How to Adjust the Framework to Fit Real Life

The 50/30/20 framework is flexible by design. In high-cost areas, needs may take more than fifty percent, especially for housing. In that case, the framework still helps by showing trade-offs rather than forcing unrealistic goals.

Some people adjust the percentages slightly, such as focusing more on savings during certain seasons of life. The framework still works as long as you understand the purpose of each category and make intentional choices. Budgeting is about control and clarity, not strict math.

Common Mistakes to Avoid

One common mistake is labeling wants as needs to avoid change. This weakens the value of the framework. Another mistake is ignoring irregular expenses, such as annual bills or occasional repairs. These should be planned for within the appropriate category so they do not cause budget surprises.

Trying to overhaul everything at once can also lead to burnout. The framework works best when applied gradually, with small improvements that last rather than large changes that fail.

Tools That Can Help You Stay on Track

You do not need advanced tools to use the 50/30/20 framework, but simple support can help. Budgeting apps, bank alerts, and monthly check-ins can keep you aware without constant effort.

Reviewing your budget once a month is often enough. The goal is to guide behavior, not to monitor every transaction. Consistent review helps the framework stay useful as your income and expenses change.

A Simple Structure for Long-Term Balance

The 50/30/20 framework offers a clear and flexible way to build a monthly budget without overcomplicating your finances. By dividing income into needs, wants, and savings, you create structure while leaving room for real life.

The framework works best when used as a guide rather than a rulebook. With honest categories and steady adjustments, it can support both daily comfort and long-term financial progress.